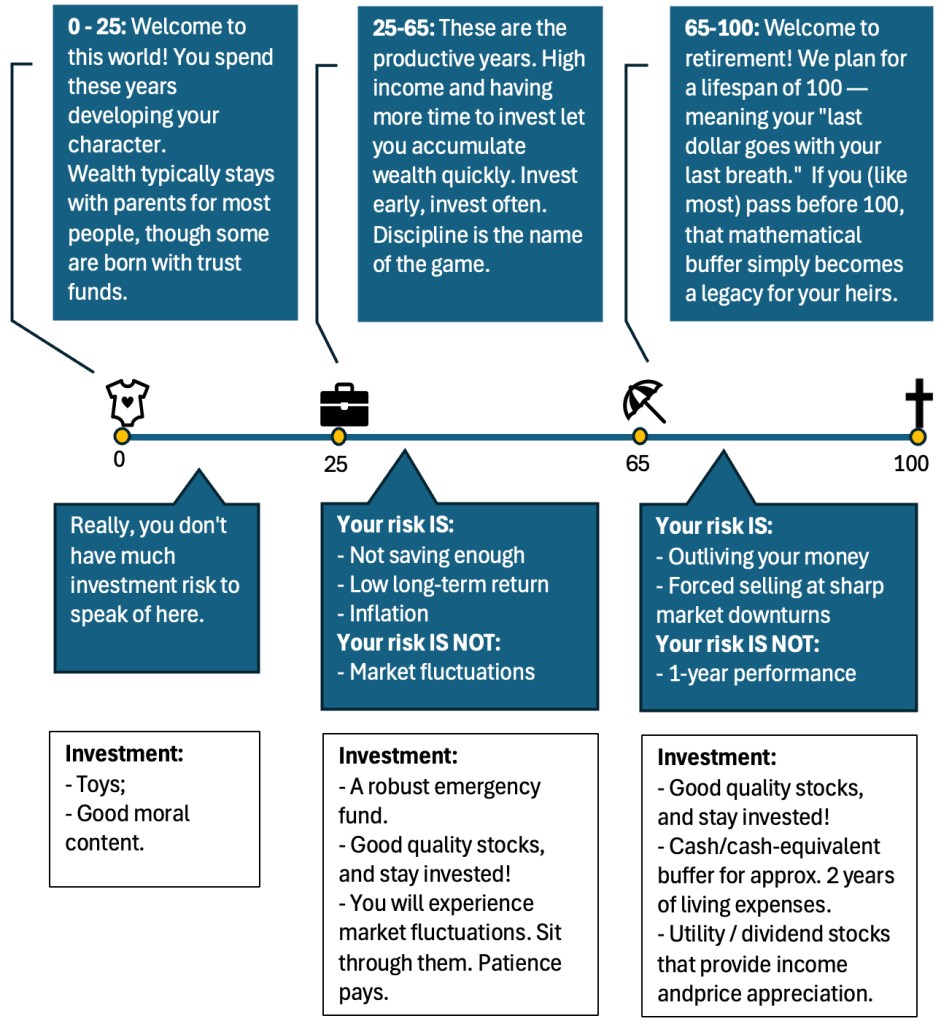

A Life-Time View at Risk

When mainstream financial media talk about “risk,” they are usually talking about short-term bumps in the road. In this context, “risk” is used interchangeably with “volatility”; it is measured using a statistical metric called “standard deviation.”

I look at things a little differently. True risk is not having enough money to afford your retirement. It is running out of money before your time here on Earth is, well, up. It is (almost) never a temporary dip in your portfolio.

Now, I invite you to look at your financial life through a long-term lens. Suppose you live to the age of 100. What are the primary risks at every stage of your life, and what strategies do we use to deal with them?

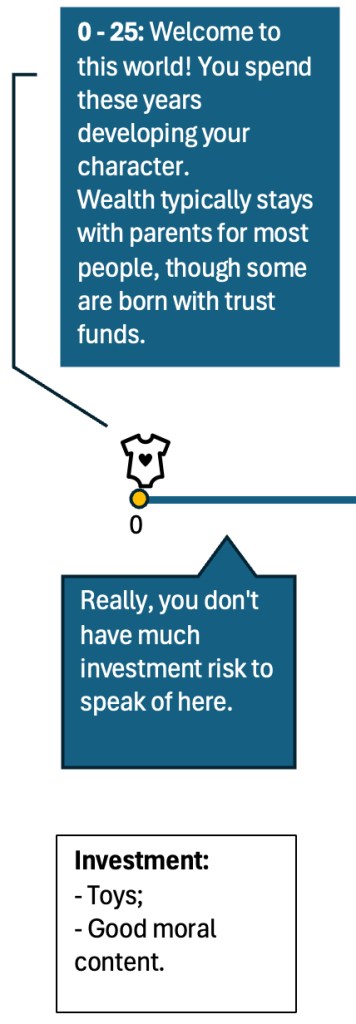

Age 0 to 25: The Foundational Years

You spend your first quarter-century developing your character and education. For most people, wealth typically stays with the parents during this phase. You don’t have much investment risk to speak of here. Your “investments” are toys, good moral content, and building the discipline you will need later.

The more fortunate ones have parents who set up trust funds for them. The even more fortunate ones start working early and set up their own Roth IRAs at a young age. Blessed is the young adult who has done this.

I have written two blogs on how putting money to work for children and young adults can really help them get a head start in life. Here are the links:

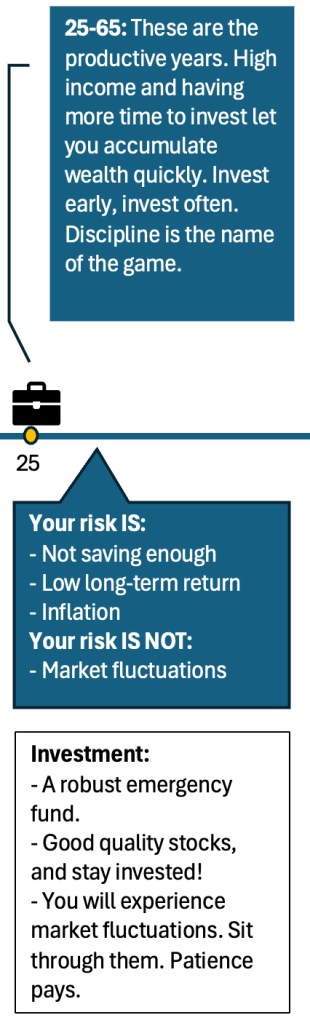

Age 25 to 65: The Accumulation Phase

These are your productive years. You have a high income and decades ahead of you, which lets you accumulate wealth rapidly.

During this phase, short-term stock market fluctuations over the next 1 to 5 years are not your risk. Your true risk is not saving enough and not generating a high enough return on your investments over these decades. Inflation will eat away your purchasing power, making it very hard to afford retirement.

The industry loves to push investors into “safe” 60/40 (stocks/bonds) portfolios to smooth out the ride. The Morningstar Andex Chart is the gold standard for visualizing why this is not such a good idea. Over a 30-year horizon, that “safe” portfolio leaves you with less than half the money you could have had.

The 2025 Andex Chart shows that if you invested $10,000 in 1995 and held it through 2024, your 30-year investment results would look like this:

- US Small Stocks: $226,600

- US Large Stocks: $224,278

- A 60/40 Global Portfolio: $100,458

(I’d love to show you a screenshot, but it is copyrighted. You can find it very easily through a quick Google search.)

Notice the stark contrast in the investment results between the 100% stock investments versus the “safe” portfolio. Playing it “safe” means giving up more than half the wealth you could have built.

Think of it this way: you are on a bumpy plane ride to the beach. That’s where the 100% stock portfolio will take you. There is another plane you can take—it is smoother, and the in-flight refreshments are amazing. But it takes you to the Gobi Desert. You can still play with all the sand you want, but it’s just not the same.

Let me repeat myself. Historically, the stock market has more up years than down years. Hiding in a safe portfolio means sacrificing your growth in the (much more abundant) good years, just so you can experience smaller drops in the (occasional) bad years.

By the way, “safe” portfolios also decline in value during those down years. I have heard it said this way: “when enough spaghetti hits the fan, everything is correlated.” In 2022, rising interest rates drove down both stocks and bonds simultaneously.

What you should do is invest early, invest often, and stay invested. When the market fluctuates, just sit through it. You should also have a good, robust emergency fund outside of the market, so when times get tight, you use that instead of being forced to sell. You will feel discomfort. It is a necessary recipe for your enduring long-term return.

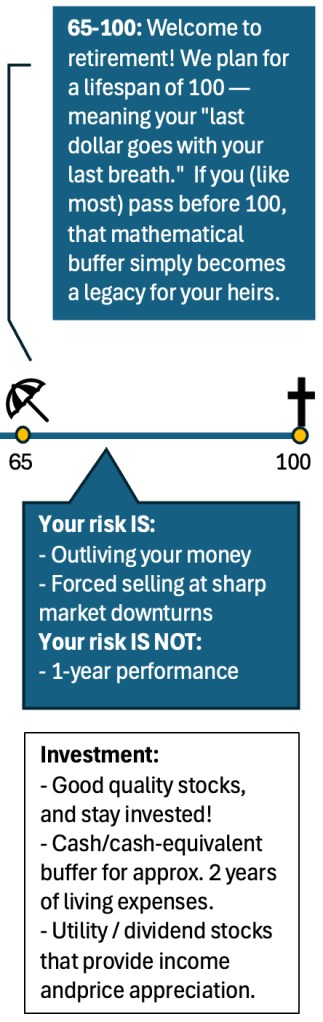

Age 65 to 100: The Distribution Phase

Welcome to retirement. We keep our financial planning process very simple—usually just two pages—and we stress-test it by assuming a lifespan of 100. Our philosophy is: with your last breath goes your last dollar. Since most people do not live to 100, that built-in buffer simply becomes a legacy for your heirs.

At this stage, a 1-year market plunge is not your true risk. Your true risk is outliving your money. The industry term for this is longevity risk.

To prevent that, we keep your core portfolio invested in quality stocks, alongside utility stocks and dividend stocks that provide excellent income while still giving you capital appreciation (typically to a smaller degree).

However, we do have to deal with the danger of a potential sharp market decline right when you retire (which is called sequence risk). The idea here is we don’t want to be forced to sell low, especially just stepping into retirement. Doing so would be detrimental to your investments lasting your entire life.

We mitigate this by ensuring you have a cash or cash-equivalent buffer for about two years of living expenses, which historically is enough time to ride out an average market recovery, while still paying you some interest.

We generally do not intentionally sell off assets just to refill this bucket, as doing so hurts your long-term compounding. Instead, we let unused dividends build up naturally, and we might occasionally shift a small portion of stock investments to safer investments when it makes sense. Or, oftentimes, clients simply hold this buffer in their own personal bank accounts.

It is also important to remember the math behind your accumulation years. If you spent the last 20 to 40 years fully invested in equities, the compounding growth you already achieved provides a strong baseline of wealth. What I mean by this is, even if a severe crash happens early in retirement, your portfolio’s value will likely still far exceed what a “safe” portfolio would have otherwise produced over that same timeframe. To put it simply, you are already ahead of the curve.

Finally, we use a dynamic approach to distributions. In our financial projections, we calculate a “target distribution” that we believe to be sustainable over the long-term. It is used to gauge what you can expect as an “income” on your savings on average. The rule is simple: if the stock market goes up, you can take out more. If it goes down, you should consider taking out less. Because there have historically been more years of up markets than down markets, this flexible approach protects your baseline wealth while keeping you comfortable. Clients usually take out less than projected simply because they don’t need it anyhow.

A Final Note on Taxes

While utilizing the appropriate tax-advantaged investment vehicles is technically a tactic rather than a high-level strategy, it is always worth mentioning. We want to be adaptive and stay tax efficient. Whether it is legislative changes or forced Required Minimum Distributions (RMDs) in retirement, you don’t want taxes quietly (and sometimes not-so-quietly) eating away at your hard-earned wealth.

Disclaimer – the content of this post is simply my opinion, and does not constitute as tax, financial, or legal advice. I simply want to put out good educational information for people. Please don’t sue me.

Leave a comment